Get a free Life Insurance quote from 20+ Canadian insurers

Getting a life insurance policy can be complicated, but the situation becomes even more difficult if you have a serious precondition. Since we often receive questions related to types of life insurance people can get when they have particular preconditions, we decided to create a user-friendly reference sheet for you. Assisting us with input on this topic is Chantal Marr, an insurance expert who has been featured in many Canadian media outlets.

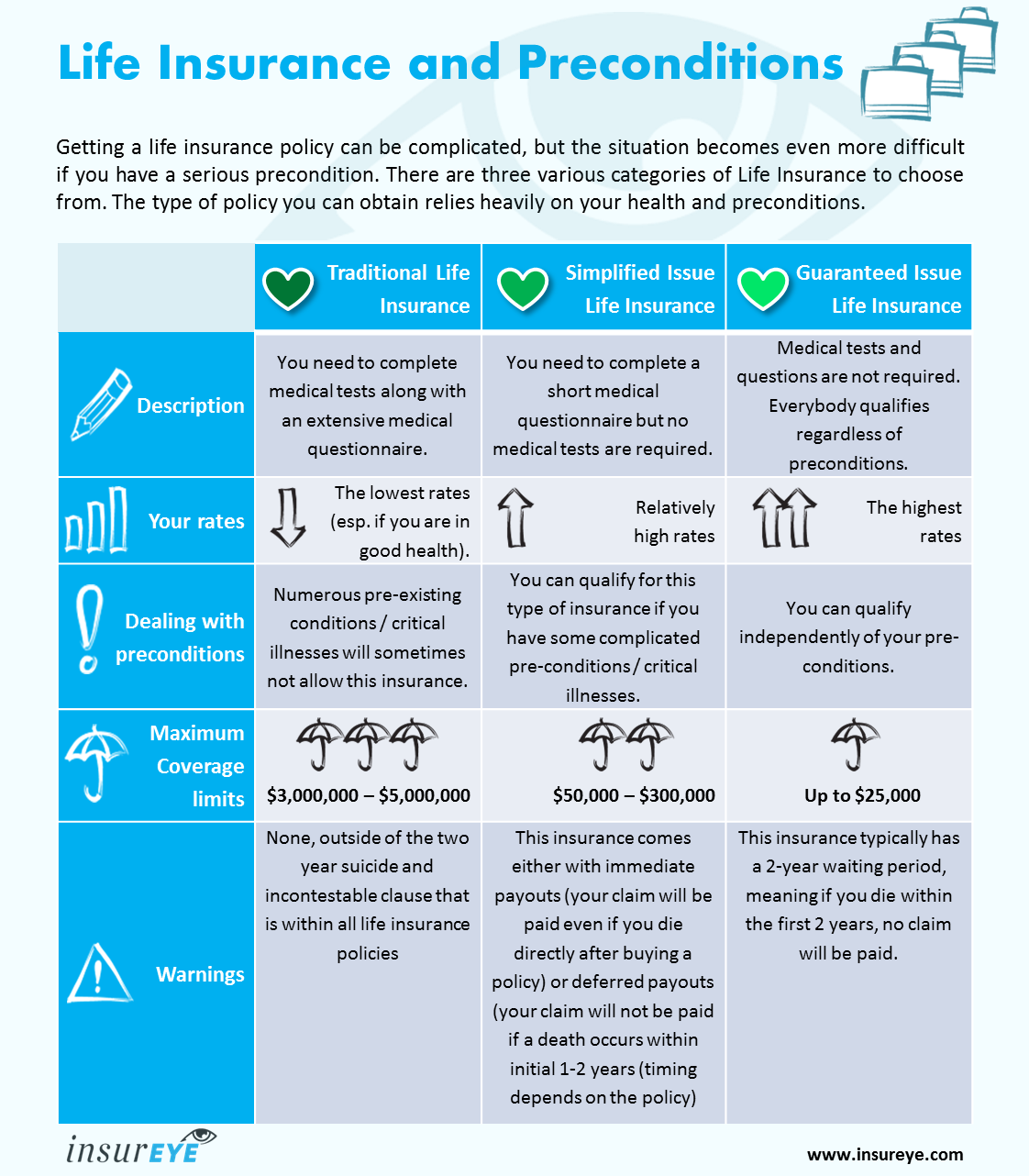

There are three different categories of Life Insurance that consumers can choose from: traditional, simplified or guaranteed issue. The type of policy you can obtain relies heavily on your health and preconditions.

The following overview details the three types of insurance products:

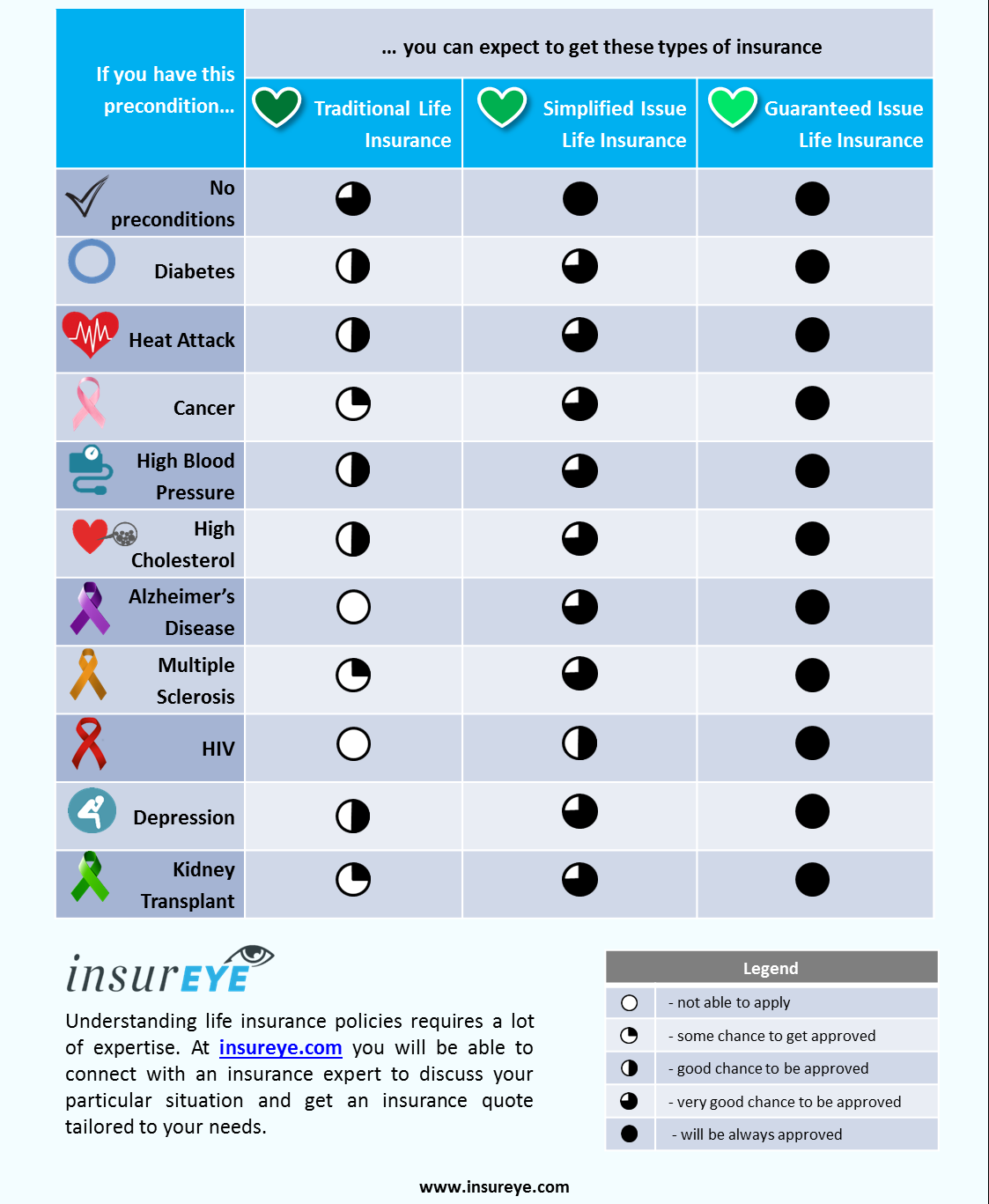

Unfortunately, not all the policies are available if you have a particular precondition. For example, people with HIV / AIDS or Alzheimer’s can not apply for standard or, also called, traditional life insurance but there are still several options available – have a look at our overview below.

Click on the link if you are interested in downloading this infographic Life Insurance with Pre-Existing Condition as PDF.

Next, we provide more insight about how insurers asses your risk. Typically there are a few important questions that either “open” or “close” the path to particular life insurance policies. Please consider that risk assessment (also called underwriting) can vary from insurer to insurer. The information below is for your general guidance only.

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Diabetes, Type 1 and Type 2 | Do you have an advanced stage of diabetes or you are insulin-dependent? | No | You can often qualify for traditional life insurance | $3,000,000- $5,000,000 | Get a quote |

| Yes | You are almost always able to qualify for simplified issue life insurance and always for guaranteed issue life insurance | $50,000 - $300,000 | Get a quote | ||

| Tip: | - Despite a frequent opinion that diabetes does not allow people to get a good life insurance policy, there are numerous insurers who are able to insure diabetes, depending on its stage. It is important to work with an insurance broker who is knowledgeable across the companies offering such services. - Type 2 diabetes is easier to insure than type 1, but the overall decision will depend on such factors as age of the applicant, blood sugar levels, treatment being in place, etc. |

||||

| Find out more: | Read more about Life Insurance for Diabetes cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Heart Attack | When did you have your last heart attack? | More than 10 years ago | You would probably be able to get traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| 1-2 years ago | You might get simplified issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Recently e.g. a few weeks ago | Expect that only guaranteed issue life insurance will be available for you. | Up to $25,000 | Get a quote | ||

| Tip: | - Before applying for traditional life insurance, you can run a so called “preliminary” inquiry, which is not formal and will give you an idea of if you qualify for traditional insurance or not. - You should be careful with trying to apply first for traditional life insurance without a preliminary inquiry because if you get rejected, you might face this question when applying for a simplified issue policy: “Have your life insurance applications been ever rejected?” You will have to answer YES, basically closing off an opportunity to get this insurance as well. Then your only option will be a guaranteed issue life insurance. If you decide to lie and answer this question as NO, you risk that your claim can be denied in future. |

||||

| Find out more: | Read more about Life Insurance for Heart Attack cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Cancer | When have you been diagnosed with cancer and what type of cancer do you have? | Long time ago (e.g. 10+ years), less serious type of cancer e.g. prostate cancer) | You would probably be able to get traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| 1-2 years ago, no changes in your condition | You are likely able to get simplified issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Just diagnosed | Expect that only guaranteed issue life insurance will be available for you. You will have a waiting period of 2 years before a claim can be made. | Up to $25,000 | Get a quote | ||

| Tip: | - Historically, cancer cases were not insurable through a traditional life insurance policy but times have changed. There are insurers that offer coverage for many cases. - It is important to work with an insurance broker who is knowledgeable across the companies offering such services. |

||||

| Find out more: | Read more about Life Insurance for Cancer cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

High Blood Pressure | If you have a high blood pressure, is it under control (no significant variations)? | Yes | You can often qualify for traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| No | You will likely qualify for simplified issue life insurance, and always for guaranteed issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Tip: | - If you manage to get your high blood pressure under control or, even better, manage to get it down, you will be able to re-apply for a re-assessment of your insurance premiums and will need to demonstrate that the situation remains positive for two years. | ||||

| Find out more: | Read more about Life Insurance for High Blood Pressure cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

High Cholesterol | If you have a high cholesterol, is it under control (no significant variations)? | Yes | You can often qualify for traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| No | You will likely qualify for simplified issue life insurance, and always for guaranteed issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Tip: | - If you manage to get your high cholesterol under control or, even better, manage to get it down, you will be able to re-apply for a re-assessment of your life insurance premiums and will need to demonstrate that the situation remains positive for two years. | ||||

| Find out more: | Read more about Life Insurance for High Cholesterol cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Alzheimer’s Disease | N/A | N/A | You can choose only between simplified issue and guaranteed issue insurance. | $50,000 - $300,000 | Get a quote |

| Tip: | - When choosing a simplified issue life insurance, you can typically choose between simplified issue with an immediate payout or with deferred payouts. The latter works very similar to guaranteed life insurance where there is usually a two year waiting time period before benefits are paid. | ||||

| Find out more: | Read more about Life Insurance for Alzheimer’s Disease cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Multiple Sclerosis | How severe is your MS stage? | Mild, applicant has control over treatment and no disabilities or other medical conditions | You can often qualify for traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| More advanced, often with a need for a caregiver | You will likely qualify for simplified issue life insurance, and always for guaranteed issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Tip: | - There are insurance companies who can insure customers with MS. It is important to work either with these companies or with an insurance broker who specializes in such cases. | ||||

| Find out more: | Read more about Life Insurance for Multiple Sclerosis cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

HIV | How advanced is the disease and is the applicant undergoing medical treatment? | Less advanced stage, applicant is able to work and also receives treatment. | You can often qualify for simplified issue life insurance. | $50,000 - $300,000 | Get a quote |

| More advanced stage, applicant might need care. | You can qualify only for guaranteed issue life insurance. | Up to $25,000 | Get a quote | ||

| Tip: | - When deciding to go with simplified issue life insurance it is important to know that it can come in the form of insurance with immediate or deferred benefits. The latter is similar to guaranteed issue life insurance which typically comes with a 24 month waiting time (i.e. if an applicant dies within the first two years, no claims will be paid). | ||||

| Find out more: | Read more about Life Insurance for HIV cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Depression | How advanced is your depression? | Mild form, stable depression. | You can apply for traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| More advanced stage, not stable. | You can qualify only for simplified issue and guaranteed issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Tip: | - With mild forms of depression you still can apply for traditional life insurance policies, and depending on your state, can be either standard or rated (can go up to 300% of standard rate). | ||||

| Find out more: | Read more about Life Insurance with Depression cases | ||||

| Precondition | Key question | Your reply | You would typically qualify for... | Maximal coverage possible | More |

|---|---|---|---|---|---|

Kidney Transplant | When did the transplant take place and how stable is the condition? | Transplant was put in place a long time ago (several years) and condition is stable. | You can apply for traditional life insurance. | $3,000,000- $5,000,000 | Get a quote |

| Transplant is recent. | You can qualify only for simplified issue and guaranteed issue life insurance. | $50,000 - $300,000 | Get a quote | ||

| Tip: | - A knowledgeable insurance broker can help you find an insurance company that insure cases with kidney transplants. | ||||

| Find out more: | Read more about Life Insurance for Kidney Transplant cases | ||||

Understanding life insurance policies requires some expertise. Make sure to use an experience life insurance broker when choosing your next life insurance or disability policy.

These insights are offered by InsurEye, a Canadian company that offers independent consumer insurance reviews and life insurance rates comparisons. InsurEye also connects consumers with experienced insurance brokers.

Carrick best reads: Seven questions to ask yourself before you retire | topfinancialnew

July 13, 2015 at 1:51 pm[…] insurance with pre-existing conditionsThis infographic was produced by the online insurance marketplace Insureye for people who want to apply for life […]

Weekend Reading - Dividend income, stock investing, diversification, pending recession and more

July 17, 2015 at 6:54 am[…] an extensive insurance infographic associated with medical preconditions courtesy of […]

Weekly Personal Finance Roundup For July 17th 2015 | Life Insurance Canada

July 17, 2015 at 5:13 pm[…] One of our online partners, Insureye.com reached out to us to help create an infographic detailing the life insurance options available to applicants with pre-exisiting medical conditions. […]

Life Insurance for People with Diabetes | Costs & Expert Tips

June 14, 2018 at 11:57 am[…] This overview will provide more details about different life insurance coverage types. […]