4 Reasons to get a Home Insurance Quote in Saskatoon

- Find out if you are overpaying today and start saving

- Request a quote from 10+ insurance providers

- Get home, tenant, house or cottage insurance including flooding coverage

- Talk to a live agent and ask any questions you want

Welcome to your home insurance guide for Saskatoon. This page will provide you with a number of useful tips for choosing home insurance protection in Saskatoon, including tips on how to get the best insurance rates.

What are average Home Insurance cost in Saskatoon?

This chart includes average rates for renter’s and homeowner’s insurance premiums in several provinces across Canada. Renters insurance premiums tend to be lower than homeowner’s insurance since renter’s insurance covers only the goods of your rented property and excludes the value of the rented property itself. Homeowner’s insurance, in contrast, does include the value of the property as it is an asset of the insured.

Saskatchewan tends to experience less liabilities due to disaster risk than other provinces. Saskatchewan does not experience earthquakes (unlike in regions of British Columbia) or massive registered floods (as can be the case in Ontario and Alberta). However, frigid winters do present a perennial risk, and pose a danger to freezing infrastructure such as home piping systems, which are prone to bursting in such conditions.

Cheap Home Insurance in Saskatoon: 10 Tips

- Wiring: Ensure the correct wiring is installed to avoid needless insurance expenses. Having approved wiring, and avoiding aluminum wiring in particular, will help keep your insurance expenses low. It’s also important to remember that some insurers will not cover houses with aluminum wiring, and when they do, a full electrical inspection is necessary.

- Plumbing insulation: Household water pipes are especially prone to freezing and bursting when the temperature drops. Insulating your pipes can be the difference between filing a claim and avoiding one.

- Water damage: Before purchasing your house, it is important to have a thorough inspection done behind and around surfaces like floors, walls and ceilings for water damage, as it can indicate water entry problems or mold.

- Change your content coverage: Check how much your coverage is for your personal effects. It may be excessive to take out a multi-thousand-dollar insurance plan if you only own economy furniture and very little valuables.

- Repair instead claims: Where possible, try to repair any small damages on insured goods yourself. Though it may be tempting to take out a claim, you may have to pay a deductible and see a rise in premiums that may cost you much more than it would had you done repairs instead.

- Annual vs monthly payments: Paying annually will often mean your premiums will be lower, since it is less complicated for the insurer to process.

- Anti-theft protection: Some insurers will note any theft alarm systems in premiums (e.g. The Personal), and reward you with a lower rate.

- Bundles: If your insurer also deals in auto and life insurance, it’s wise to inquire about possible bundle discounts.

- Hydrants and fire-station: Ask your insurer if proximity to fire hydrants or a fire station will lower your premiums.

- Stability of residence: If you have lived in the same residence for years, some insurers may view you as a stable applicant, and will offer you a stability discount.

5 Elements that will increase your House Insurance costs

- Finished basement: Finished basements are expensive to repair if flooding occurs, so while a finished basement adds to the value of the home, it can also add to your premium.

- Building frame: Wood frame homes are more likely to suffer from fire, so they may be considered less safe than concrete or brick homes. As such, wood frame houses may face higher insurance costs.

- Swimming pools: Pools represent higher liability, especially when not protected by a fence. In the eyes of insurers, it is an additional liability that can be very costly.

- Roof type: Different roof types are not seen as equal by insurers and that reflects in insurance premiums. The least reliable roofs are wood shake or shingle.

- Garden and Trees: Having a garden, including fencing, is not considered a higher risk just because you have them; but in most cases you do have to pay extra for this type of coverage.

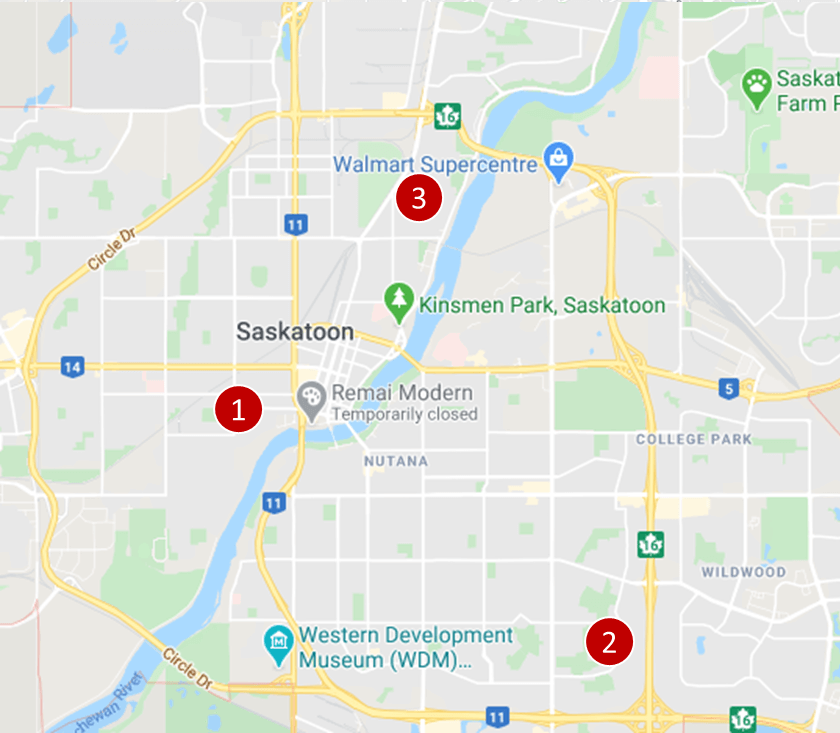

Saskatoon Home Insurance quotes, examples

Saskatoon home insurance quote #1: Homeowners insurance for a 2-storey detached house located next to Optimist Park. This is a house under 1,000 sq. ft, has an attached single-car garage, no basement, and a wooden frame.

Price: $124 per month ($1,488/year)

Saskatoon home insurance quote #2: Tenants home insurance for a 1-storey detached house. Square footage under 1,000 sq. ft, no garage, no basement, a new roof, located on East Dr. next to James Anderson Park.

Price: $24 per month ($288/year)

Saskatoon home insurance quote #3: Homeowners insurance for a 1-storey detached house under 1,000 sq. ft; a new roof, no basement, no garage, located in a North Park neighborhood, next to the intersection of Edward Ave and Balmoral St:

Price: $91 per month ($1,092/year)

5 Home Insurance myths to know

Myth #1: Insurance is cheaper for older, less expensive homes.

Intuition may cause you to think that, because your home is older and less valuable, homeowner’s insurance premiums will follow suit, but this is not the case. In fact, insurance for these properties is typically more expensive because aging properties are more prone to having wiring not up to code or use old and outdated plumbing systems that become compromised with time. These factors produce in increased probability of a disaster claim.

Myth #2: If I have a home insurance policy, I am protected against sewer backup.

Municipal infrastructure tends to be very efficient but can fall short due to shocks like flooding. During heavy rain and floods, sanitary and storm sewer systems can back up because they cannot handle the influx of water, leading to backup in toilets and drains. Most insurers will offer optional sewer backup protection, but it is important to remember that this eventuality is usually not covered by standard homeowner’s insurance policies. Check to see if your provider does include it in their standard policy, and how you can attain it if they do not.

Myth #3: If I am away on vacation, my house is covered.

Failure to account for certain precautions can void your coverage in the event of a disaster while you are away on vacation. So, if you leave (especially during the winter) make sure you do one of these two things:

- Shut off the water supply to your house, then drain all the pipes, or;

- See that your home’s heating is maintained for the duration of your vacation.

You may not be covered against water damage if your pipes burst without this due diligence. Before you leave, consult your provider to learn what length of vacation will require you to take these precautions, and perhaps arrange for someone to check up on your home periodically while you are away. Typically, this should be done every three to seven days, though policies regarding these visits may differ.

Myth #4: If a car is stored in a garage, it is covered by the home insurance policy.

Your vehicle is not covered by your home insurance policy. It is covered by the comprehensive coverage of your auto insurance policy.

Myth #5: All home insurance policies are the same.

Each policy from each provider will differ in what they cover and what protection types they offer. There are likely significant differences in factors such as handling of water damages (from flooding or a sewage backup), the amount of coverage, and the living expenses cap.

Coverage for homeowners insurance in Saskatoon depends on the type of insurance you need.

- Tenants insurance: Tenants, also known as renter’s, insurance covers your unit’s contents, storage locker, and liability.

- Homeowners insurance (house): Robust coverage that includes the rebuilding value of your home along with liability and some protection for natural disasters (other disasters like floods, earthquakes, and landslides can be added via riders if not included).

The cost of homeowners insurance in Saskatoon depends on the risk profile of your home and property, and the type of dwelling in which you live.

- Tenant insurance is the cheapest. It can be as little as $20/month.

- Homeowners insurance for a house varies because it depends on many factors like the size of the home, the location, the risks in the area (flooding, earthquakes, etc.) the condition/maintenance of the home, the type of wiring, the presence of a fire place and more. For many regular size homes (1,000 – 2,000 sq. feet) in decent condition, the insurance costs will be in the ballpark of $70 – $150/month. Should homes have completed basements with some flooding risk or/and serious house maintenance issues (e.g. old roof) or additional hazard associated with a home (e.g. high-risk fireplaces, etc.), the costs might exceed $150 / month.

It is important that you look for additional coverage (e.g. jewellery, collectibles, or business equipment/assets if your business operates from home), as these items may exceed your contents coverage limits.

Also, details of your coverage (e.g. level of deductibles, coverage limits, etc.) will impact the final price.

Since different insurers specialize in different demographics, the best way to get the cheapest home insurance in Saskatoon is to compare a variety of quotes from several companies. Some companies focus on rural properties, others in condos. Some cover seniors or affiliated groups.

There are some property and casualty insurers who are focused more on particular provinces in Western Canada including Saskatchewan (e.g. SGI, Peace Hills Insurance). Other providers are active Canada-wide (e.g. Intact, Aviva, TD Insurance).

Our insurance professionals have access to more than 30 Canadian insurance companies and will, for free, compare the market on your behalf and present you with the best quotes for the coverage you need.

Our proprietary insurance review platform has been collecting independent consumer reviews since 2012 for all types of insurance and financial products. Click here for free access to thousands of reviews.

Our Publications related to Home Insurance

Introducing a New Tool to Find Out What Issues Canadian Face with Their Insurers

The arrival of COVID-19 has pushed Canadians, more than ever before, online for finding and applying for insurance and banking products. It is not easy, though, to make the right choice without knowing if a particular insurer will be there when you need them the most. As the largest Canadian review platform with thousands of […]

How Much a Good Condo View is Worth Today?

A prospective buyer is always going to be focused on a condo unit’s view. Unlike a house, these units rarely have multiple windows to the outside in various directions. The exterior wall, which usually is either glass or contains a balcony, is likely the only point of contact with the natural world. While the interior […]

Own your home? You could be eligible for these tax credits and rebates

It’s no secret that property prices in many urban areas of Canada are on fire. And it’s not limited to just the core of Toronto and Vancouver. Houses for sale in Hamilton, for example, have doubled in price in the last decade and houses in Mississauga are almost $750,000. It’s increasingly hard for the average […]

How Competitive is it to Buy a Home in Toronto? INFOGRAPHIC

Toronto real estate has been tumultuous in the last few years. At first, everything was going, up, up and up. Record low-interest rates made huge mortgages more attractive, and few new suburbs were developed thanks to the Greenbelt. Almost 90, 000 Newcomers were moving to Toronto each year, along with Canadians from other parts of […]

Canadian Condo Review Platform CondoEssentials Launched

InsurEye Inc has announced the launch of a new website: CondoEssentials. The new site is a condo review platform that has been designed to better inform Canadians about real estate, with a particular emphasis on condominiums. InsurEye has been informing consumers about details of auto, life and condo insurance for years through thousands of independent […]

| Home Insurance in Ontario | ||